Trust & numbers

Trust is built before money moves.

Brolly is simple on the surface: borrow, lend, repay. Underneath it needs identity checks, consented bank data, payment rails, servicing paths and risk language that does not flinch.

Borrowing is subject to eligibility, affordability, product availability and lender matching. Lending involves risk, including delayed repayment, default and possible loss of capital.

Live trust stack AU

Important Lending involves risk including possible loss of capital. Brolly is not a bank.

Numbers, then warnings

Proof helps. It does not remove risk.

Numbers should make the product easier to understand, not easier to oversell. The useful pattern is simple: show the product shape, then keep the downside on the same page.

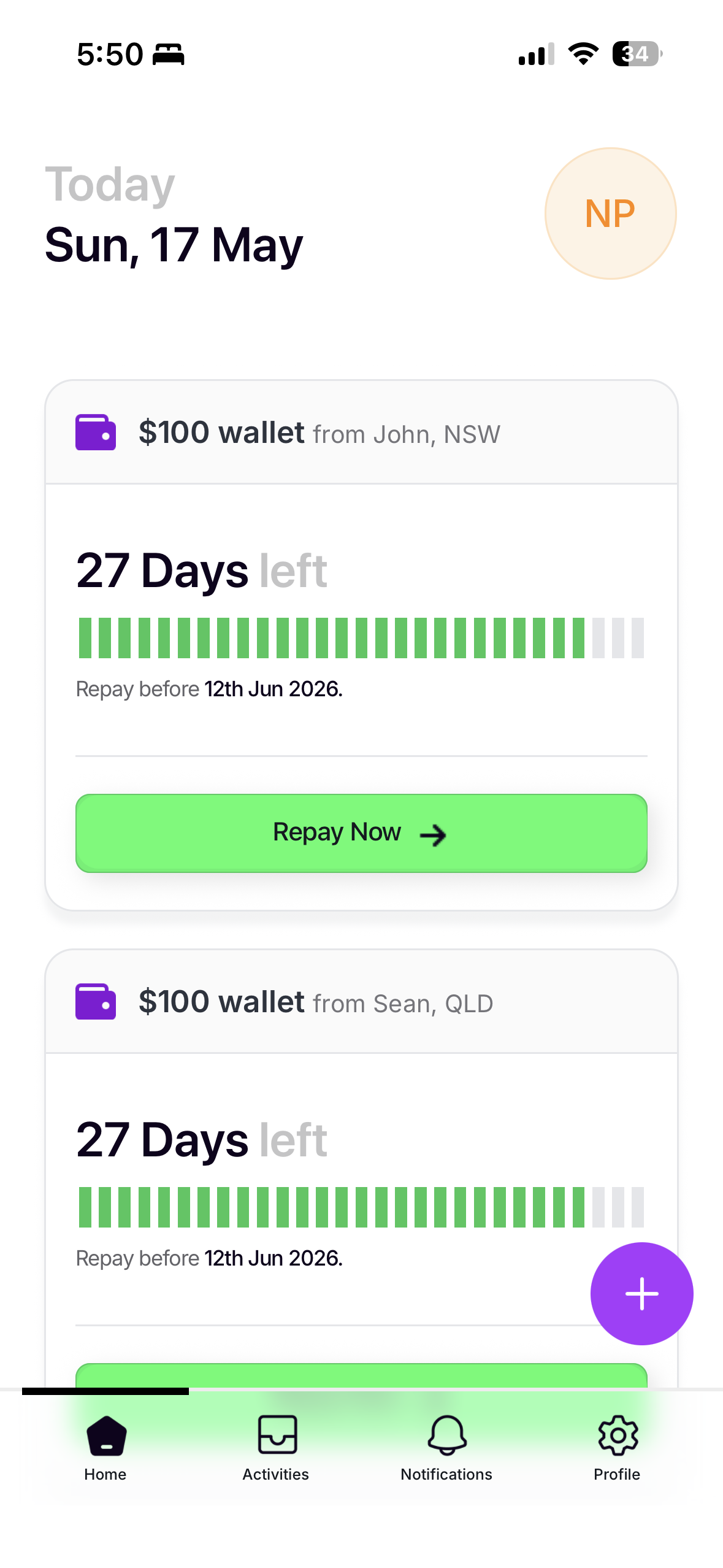

Live product

iOS public beta and a real short-term lending loop — not just a concept page.

1:1 structure

Each loan is matched borrower to lender. The page does not hide behind a pooled-fund story.

Risk shown early

Return, default, liquidity and Financial Claims Scheme warnings sit near the proof, not buried at the bottom.

Partner rails

Identity, bank-data, payments and collections run through named operating partners.

Underwriting

Not just a credit score and a prayer.

Brolly’s trust story starts before matching: identity, consented bank data, affordability and repayment-cycle controls. That is the boring machinery a short-term credit app has to get right.

This page avoids pretending technology eliminates risk. It should show the checks, then say what the checks cannot guarantee.

Identity

FrankieOne supports identity checks before borrowers move through the flow.

Bank data

Basiq-supported bank-data rails help assess income, spending and cash-flow patterns.

Affordability

Brolly checks whether the requested loan can fit the borrower’s short-term position.

Repayment loop

Borrowers need to repay and close the current cycle before reapplying.

Rails underneath

Simple app. Named rails.

Cash-App-style does not mean vague. The page names the operating layers that make the app feel simple: identity, bank data, payments, servicing and recovery.

Risk in plain English

The warning belongs beside the proof.

Lender returns can be attractive only if the risk is visible. Brolly should not sound guaranteed or government-backed. It is lending. Lending has downside.

Capital can be lost

Borrowers can repay late or default. Lender capital is at risk.

Returns are variable

Target returns are not guaranteed. Borrower repayment behaviour and platform operations matter.

Not a bank

Brolly is not a bank. Funds are not covered by the Australian Government Financial Claims Scheme.

Assurance is limited

Any Assurance Account is a discretionary reserve, not insurance or a contractual guarantee.

Important. Lending on Brolly involves risk including possible loss of capital. Brolly is not a bank. Funds are not covered by the Financial Claims Scheme. Returns are variable and not guaranteed. Do not lend capital you cannot afford to lose. Consider seeking independent financial advice if you are unsure.

Next

Open the app. Complete KYC before money moves.

Borrowers and lenders start in the iOS app. After KYC, users can choose whether to borrow or lend — with risk still shown plainly before capital is deployed.