Complete identity verification and accept the lender terms. Onboarded in minutes.

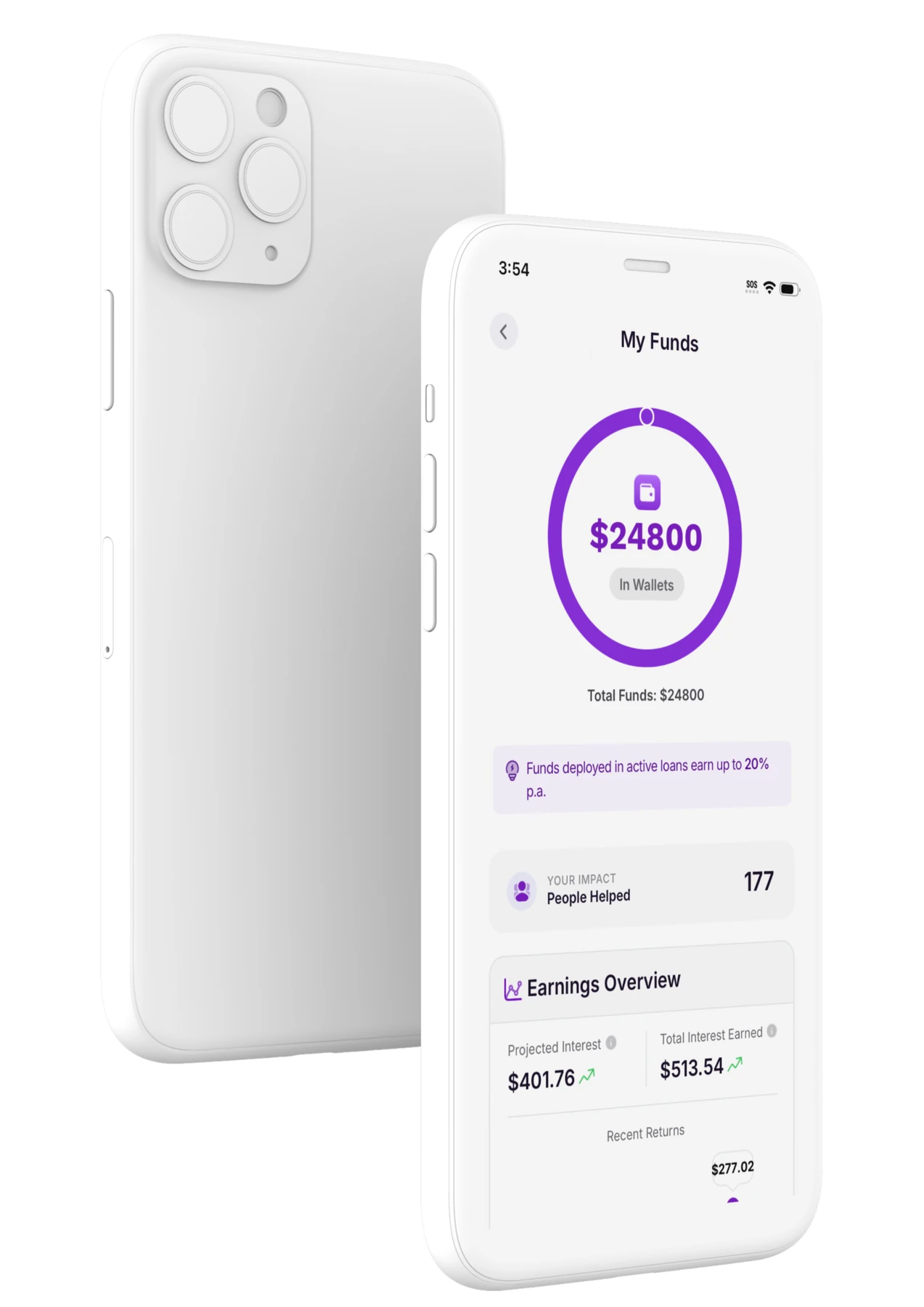

Lending in app

Build a diversified loan portfolio, managed end to end.

Brolly's intelligent decisioning engine handles credit assessment, deployment,matching, repayment and recovery. End-to-end, fully automated.

12% p.a. is a target, not a guaranteed return. Lending has risk: repayments can be late, delayed, unpaid, or capital can be lost. Read lender FAQ →

How it works

Verify. Fund. Deploy. Earn.

Onboard, fund your wallet, set your deployment preferences and let your capital cycle.

Add capital to your Brolly wallet. PayID transfers settle instantly via Monoova.

Auto-Deploy matches your capital to pre-qualified borrower loans, diversified across multiple positions.

Capital cycles on 30-day loans. Returns credited to your wallet. Idle funds liquid 24/7. Track every position in real time.

Live activity

Real people. Real loans. Right now.

Risk-managed in real time. Machine learning scores every loan on live bank data and behavioural signals before capital deploys. Live decisioning throughout the cycle.

Illustrative activity, representative of platform behaviour. Names anonymised. Actual platform activity is private.

How your capital works

Many borrowers. One wallet.

Every dollar in your Brolly wallet gets matched to verified borrower loans, capped at A$2,000 per borrower. As your balance grows, your capital spreads across more loans. Diversification is built in, not optional.

Illustrative diversification. Actual borrower count varies by deployment cadence and loan availability.

Why Brolly

Visibility, control, automation.

Diversified by default.

Your capital is spread across multiple matched loans automatically. Concentration risk managed without you lifting a finger.

Loan-by-loan visibility.

Every match is visible by amount, status and cycle. No pooled product. No hidden positions.

Capital states, never hidden.

Every dollar shown as idle, deploying, active or returned. Real-time wallet states throughout the cycle.

Risk-managed in real time.

Machine learning scores every loan on live bank data and behavioural signals before capital deploys. Live decisioning throughout the cycle.

Performance

Performance matters.

Realised yield to marketplace lenders over the 12 months to May 2026. The HNW Marketplace pathway targets 12% p.a. Historical performance is not indicative of future results. The platform maintains a >95% capital deployment ratio, with 0% lender losses and an average default rate of 2%.

Built on institutional infrastructure

Infrastructure

Five rails under the process.

Provider names stay readable. The page stays simple.

FrankieOne Identity, KYC, AML and fraud Brolly risk engine Decisioning Monoova Payments and repayment

Runs identity verification, compliance checks and fraud screening before a borrower can progress.

Basiq Open banking affordabilitySupplies live bank-data signals so Brolly can assess affordability from transaction behaviour.

Evaluates behavioural and transactional features against Brolly's proprietary risk model and product rules.

Handles disbursement and repayment automation through the New Payments Platform.

InDebted RecoverySupports tiered recovery activity for loans that move beyond Brolly's recovery threshold.

Risk in context

Where Brolly sits in Australian consumer credit.

Australian residential mortgages

1.07%

Brolly marketplace

1.43%

Unsecured lending (industry segment)

~2.0%

Australian unsecured personal loans

~5.0%

Sources: RBA financial stability data, ASIC consumer credit reports, comparable lender disclosures. Methodology varies by source.

FAQ

What lenders ask first.

Learn more about being a community lender.

What is my security?

Lenders deploy capital directly into live consumer loan receivables. Every loan is asset-backed by the borrower's repayment obligation, supported by Open Banking affordability data, automated repayment rails (Monoova) and a tiered recovery pathway (InDebted). The Assurance Account sits behind the book as a discretionary buffer.

What are the lender losses to date?

Zero lender capital losses since launch. 3,000+ loans funded over 12 months of live operation. Historical record, not a forecast. Around 30% of completed borrower applications are declined based on affordability, identity or risk-engine outcomes, before any lender capital is deployed.

How does the Assurance Account work?

A discretionary reserve funded from Brolly's platform margin. It sits behind the loan book as a buffer against principal loss. Not insurance, not a guarantee, not government-backed.

What happens if Brolly stops operating?

Lender wallet balances sit in segregated client funds through Monoova (an AFSL-licensed payment provider), separate from Brolly's corporate accounts. Active loans remain legally enforceable obligations between borrower and lender. Recovery continues under the existing servicing arrangements.

What's the biggest drag on realised returns?

Late repayments, more than defaults. Delays reduce capital velocity and therefore compress realised yield through slower recycling of capital.

How concentrated is the loan book?

Loans cap at A$2,000 per borrower and average closer to A$500. Allocator capital is naturally diversified across thousands of small positions, not concentrated in a few large ones.

How quickly can capital be accessed?

Marketplace positions return at cycle maturity (typically 30 days), supporting regular liquidity events. Idle wallet funds remain fully withdrawable at any time.

Platform economics

How lender returns are funded.

~60%Gross p.a.

Borrowers pay a fixed service fee. That fee funds targeted lender returns and the operating layer behind each loan.At full recycling, a 5% monthly borrower fee can equal about ~60% gross annualised platform revenue before defaults, funding costs and expenses.Marketplace lenders target about ~12% p.a. The remaining gross margin pays for risk, servicing, payment rails and platform growth.

Start

Start lending today.

Real returns. Real impact. A community of Australians.